Debt Consolidation in Canada – When It Helps and When It Doesn’t

December 05, 2024

Debt Consolidation in Canada

Last Updated: July 2026

Debt consolidation in Canada can help borrowers combine several debts into one monthly payment. It may lower interest costs, simplify budgeting, and create a clearer repayment plan. But it does not work for everyone.

A debt consolidation loan can be helpful when the new loan has a lower interest rate than your current debts, the payment fits your budget, and you stop adding new debt. It can be a poor choice when the loan has a higher rate, a much longer term, hidden fees, or when you continue using credit cards after consolidating.

This guide explains how debt consolidation works in Canada, when it helps, when it does not, how to calculate whether it can save you money, and which alternatives may be better if your debt has become unmanageable.

If you are comparing borrowing options, you can also review our page on debt consolidation loans in Canada.

Who This Guide Is For

This guide is for Canadians who are dealing with several debts and want to understand whether debt consolidation is the right next step. It may be useful if you have credit card balances, personal loans, store cards, lines of credit, or installment loans and want one clearer repayment plan.

It is also for borrowers who are unsure whether consolidation, credit counselling, a debt management plan, a consumer proposal, or bankruptcy is the better option.

Editorial Standards

This article is reviewed regularly to reflect Canadian lending rules, consumer protection guidance, and current debt repayment options. FatCat Loans is a loan comparison platform, not a lender or debt counselling agency. This guide is for general information only and should not replace professional financial or insolvency advice.

Contents

- What is debt consolidation?

- How debt consolidation works

- When debt consolidation helps

- When debt consolidation does not help

- What debts can you consolidate?

- How to calculate whether consolidation saves money

- Types of debt consolidation options

- Alternatives to debt consolidation

- Common mistakes to avoid

- Frequently Asked Questions

Debt Consolidation in Canada at a Glance

| Feature | What It Means |

|---|---|

| Main purpose | Combine several debts into one payment |

| Best for | Borrowers with stable income and manageable debt |

| Common debts | Credit cards, store cards, personal loans, lines of credit |

| Main benefit | Simpler repayment and possible interest savings |

| Main risk | Paying more if the rate is high or the term is too long |

| Important reminder | Debt consolidation does not erase debt |

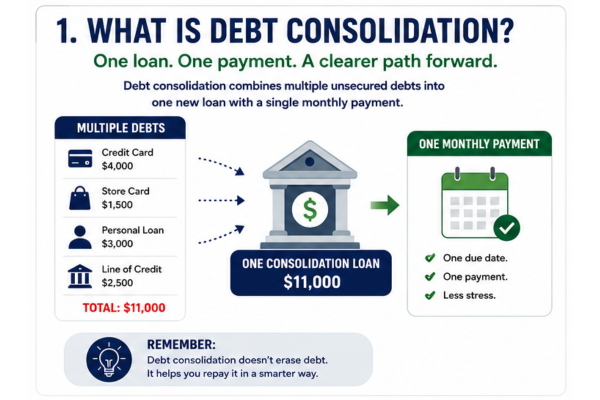

What Is Debt Consolidation?

A debt consolidation loan is a new personal loan used to pay off several existing unsecured debts at once. Instead of multiple balances and due dates, you end up with one loan, one payment, and one repayment timeline.

What it isn’t: consolidation doesn’t “erase” debt, and it isn’t the same as debt forgiveness, a consumer proposal, or bankruptcy. You’re still repaying what you owe — just in a simpler structure that can be easier to manage.

If you’re also comparing ongoing borrowing options, a personal line of credit can work differently than a debt consolidation loan.

What Is a Debt Consolidation Loan?

A debt consolidation loan is a personal loan used to pay off several unsecured debts. Instead of paying multiple lenders every month, you make one payment toward the new loan.

These loans typically consolidate:

- Credit card balances

- Personal loans

- Retail or store credit cards

- Personal lines of credit

- Short-term or installment loans

- Overdue bills or other unsecured debts

The goal is simplicity — and ideally, savings.

How Debt Consolidation Works in Canada

Here’s the typical process for getting a debt consolidation loan in Canada:

- List your existing debts — balances, interest rates, and payments.

- Compare lenders to find competitive debt consolidation loan rates.

- Apply and provide documentation, such as income and ID.

- Receive loan approval and funds, based on credit and affordability.

- Use the new loan to pay off multiple existing debts.

- Make one monthly payment toward the debt consolidation loan until paid off.

When Debt Consolidation Helps

Debt consolidation can be a smart move when it improves your financial position instead of only moving debt around. The goal should be to make repayment simpler, cheaper, or more structured.

1. You qualify for a lower interest rate

Debt consolidation is most helpful when the new loan has a lower interest rate than the debts you are paying off. This is common when borrowers use consolidation to replace high-interest credit card debt with a lower-rate personal loan.

For example, if you are paying 20% to 29% on several credit cards and qualify for a debt consolidation loan at a lower rate, more of your payment may go toward reducing the balance instead of covering interest.

2. You want one clear monthly payment

Managing several balances, due dates, and minimum payments can be stressful. Consolidation can make budgeting easier because you know exactly when the payment is due and how long repayment should take.

3. You have stable income

Consolidation works best when your income is steady enough to cover the new monthly payment. Lenders usually want to see that the payment is affordable after rent, utilities, food, transportation, and other debt obligations.

4. You are serious about stopping new debt

Consolidation can only help if you avoid building new balances after the old debts are paid off. If you consolidate credit cards and then start using those cards again, you may end up with both the new loan and new credit card debt.

5. You want a fixed repayment timeline

Credit card debt can last for years if you only make minimum payments. A debt consolidation loan usually has a fixed term, which means there is a clear end date if you make every payment on time.

When Debt Consolidation Does Not Help

Debt consolidation is not always the right solution. In some cases, it can make debt more expensive or delay a deeper financial problem.

1. The new rate is not lower

If the debt consolidation loan has the same or higher interest rate than your current debts, it may not save money. It may still simplify payments, but the total cost could be higher.

2. The repayment term is too long

A longer term can reduce your monthly payment, but it may increase the total interest paid. This is one of the biggest mistakes borrowers make. A lower payment is helpful only if the full repayment cost still makes sense.

3. You keep using your credit cards

Debt consolidation can free up credit card limits. That can be risky. If you use those cards again, you may double your debt instead of reducing it.

4. Your budget is already too tight

If you cannot afford your basic expenses, consolidation may not be enough. You may need credit counselling, a debt management plan, a consumer proposal, or another debt relief option.

5. You are borrowing to delay insolvency

If you are missing payments, receiving collection calls, or using one loan to pay another, consolidation may only delay the problem. In that case, speaking with a non-profit credit counsellor or Licensed Insolvency Trustee may be more appropriate.

What Debts Can You Consolidate?

Debt consolidation is usually used for unsecured debts. These are debts that are not tied to an asset such as a home or car.

| Debts You Can Usually Consolidate | Debts That May Not Be Suitable |

|---|---|

| Credit card balances | Mortgage debt |

| Store cards | Car loans secured by a vehicle |

| Personal loans | Government student loans in some cases |

| Personal lines of credit | Child or spousal support arrears |

| Installment loans | Certain tax debts |

| Unsecured bills or accounts | Debts already in legal action |

If you are unsure whether a debt can be consolidated, check with the lender before applying. Some lenders may pay creditors directly, while others may deposit funds into your account so you can pay the balances yourself.

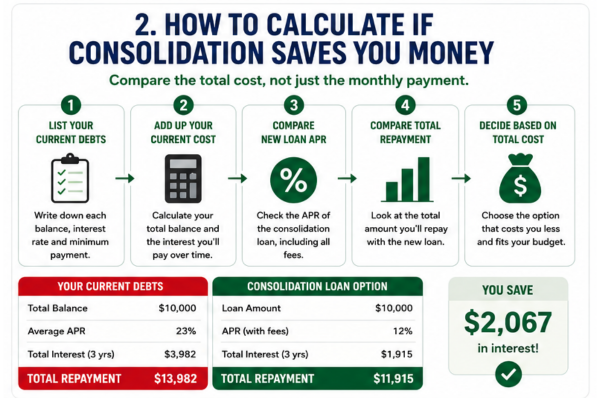

How to Calculate Whether Debt Consolidation Will Save Money

To know whether debt consolidation will actually help, compare the total cost of your current debts with the total cost of the new loan.

Step 1: List each current debt

Write down the balance, interest rate, minimum payment, and estimated payoff time for each debt.

Step 2: Work out your current weighted average rate

If most of your debt is on high-interest credit cards, your average rate may be high. If some debt is already low-interest, consolidation may not save as much.

Step 3: Compare the new APR

Do not compare only the interest rate. Compare the APR and total cost of borrowing, including any fees.

Step 4: Compare the total repayment amount

A lower monthly payment does not always mean a cheaper loan. Look at how much you will repay over the full term.

Example: When consolidation may save money

| Current Debt | Balance | APR |

|---|---|---|

| Credit card 1 | $4,000 | 22% |

| Credit card 2 | $3,500 | 20% |

| Store card | $2,500 | 29% |

| Total | $10,000 | High average rate |

If you qualify for a $10,000 debt consolidation loan at a lower APR and keep the term reasonable, you may reduce interest costs and create a clearer payoff plan.

Example: When consolidation may not save money

| Scenario | Why It May Not Help |

|---|---|

| New loan has a higher APR | You may pay more interest |

| Term is stretched too long | Lower payments may increase total cost |

| Fees are high | Upfront costs may reduce savings |

| You keep using credit cards | You may create new debt |

Before accepting a loan, use a loan calculator or ask the lender for the full repayment schedule. You can also compare options through our loan calculator if you want to estimate payments before applying.

How do debt consolidation loans work in real life? A simple example

Let’s say you’re currently making three payments:

• Credit card: $3,500 balance at a high interest rate

• Store card: $1,200 balance

• Personal line of credit: $4,000 balance

You’re paying different due dates and (often) different interest rates. A debt consolidation loan combines those balances into one new loan amount (example: $8,700 plus any applicable lender fees). You then make one monthly payment to the new loan.

The goal is usually one or more of the following:

• reduce your total monthly payments (better cash flow)

• secure a lower overall cost of borrowing (less interest over time)

• create a clear end date so the debt actually gets paid off

Important: the “best” debt consolidation loan isn’t always the lowest monthly payment. A longer term can lower the payment but raise the total interest paid.

If approved at a lower interest rate or shorter term, you may pay off debt sooner and spend less on interest overall.

Benefits of Debt Consolidation

✅ One monthly payment instead of multiple bills

✅ Potentially lower interest rates, depending on credit profile

✅ Predictable payments with a fixed term and schedule

✅ Reduced financial stress and clutter

✅ Improved ability to budget and plan ahead

✅ May protect or improve credit, if payments remain on time

For borrowers committed to repayment, consolidation can provide structure and momentum toward becoming debt-free.

Who Should Consider Debt Consolidation?

Debt consolidation is best suited to borrowers who have enough income to repay their debt but need a better structure.

You may be a good candidate if:

- You have several high-interest unsecured debts.

- You can qualify for a lower rate than you currently pay.

- You have stable income.

- You want one fixed monthly payment.

- You are ready to stop relying on credit cards while repaying debt.

- You can afford the new payment without missing bills.

You may want to consider other options if:

- You are already missing payments.

- Your debts are mostly in collections.

- You cannot afford basic living costs.

- You need to borrow more money to keep up with current debt.

- Your total debt is too high compared with your income.

If your credit score is making approval difficult, you may want to compare bad credit loan options alongside debt consolidation loans to understand what rates and terms may be realistic.

Risks and Considerations

While helpful, debt consolidation loans aren’t ideal for everyone:

❌ Approval may require good credit, stable income, or low debt ratios

❌ Longer repayment terms may increase total interest paid

❌ Continuing to use credit cards can create more debt

❌ Consolidation does not erase debt — it reorganizes it

❌ Upfront fees or penalties may apply, depending on lender

To avoid falling back into debt, many borrowers pause or limit credit card use during repayment.

For additional government guidance on managing debt and evaluating consolidation, the Financial Consumer Agency of Canada offers unbiased education and resources.

Debt consolidation loan checklist (before you accept an offer)

Before you accept any debt consolidation loan, confirm these items in writing:

- Total cost of borrowing: total interest + any fees over the full term

- APR vs interest rate: APR includes certain fees and reflects the true cost

- Term length: shorter terms usually cost less overall, but payments are higher

- Prepayment rules: confirm you can pay extra or pay off early without penalty

- Funding method: will the lender pay your creditors directly or deposit to your account?

- Reporting: does the lender report payments to a credit bureau? (this can help build positive history if you pay on time)

For consumer guidance on borrowing costs, affordability, and avoiding high-risk offers, this is a helpful reference: Financial Consumer Agency of Canada.

How to Apply for a Debt Consolidation Loan

To improve your chances of approval and lower rates:

- Check your credit score and report for accuracy.

- Calculate how much debt you want to consolidate.

- Compare lenders in Canada — banks, credit unions, online lenders, and loan marketplaces.

- Review APR, term length, fees, and total cost.

- Apply and submit supporting documents, such as proof of income.

- Use loan funds responsibly — directly pay off outstanding debts.

- Stick to a repayment plan and avoid new debt during the term.

Tip: Many lenders offer pre-qualification with a soft credit check — helpful before applying, to avoid your credit score from being affected.

Documents you’ll typically need (so you don’t get delayed)

To keep the process moving, have these ready:

• Government ID

• Proof of income (pay stubs, benefits statements, or bank deposits)

• Proof of address

• List of debts (balances, lenders, and account numbers if the new lender pays creditors directly)

• Recent bank statements (sometimes requested to verify affordability)

Being prepared can speed up verification and funding.

What lenders look at for a credit consolidation loan in Canada

Most lenders evaluate the same core areas when deciding approval and pricing:

• Income and stability: consistent pay is a major factor

• Debt-to-income ratio: how much of your income is already committed to debt payments

• Credit profile: score, late payments, utilization, collections, and recent inquiries

• Banking history: NSF patterns and overdraft frequency can matter

• Loan purpose and amount requested: lenders price risk differently depending on the total amount

Tip: if your credit is recovering, you may still qualify — but the interest rate could be higher. If that’s your situation, compare options carefully and prioritize lenders that clearly disclose the total cost up front.

If your credit score is lower, some lenders still offer consolidation options by focusing more on income and affordability rather than credit history. In these cases, comparing bad credit loans alongside debt consolidation loans can help you understand realistic approval terms and total borrowing costs.

Types of Debt Consolidation Options in Canada

Debt consolidation does not always mean one type of loan. Canadians may have several options, depending on credit score, income, home equity, debt type, and repayment goals.

1. Debt Consolidation Loan

A debt consolidation loan is a personal loan used to pay off multiple debts. It usually has a fixed payment, fixed term, and clear end date. This can be helpful if you want structure and predictable repayment.

This option may work well if you qualify for a lower rate than your current debts. It may not work well if the rate is high or if the payment does not fit your budget.

2. Balance Transfer Credit Card

A balance transfer credit card lets you move credit card debt to a new card, often with a low promotional interest rate for a limited time. This can help if you can repay the balance before the promotion ends.

It may not help if you only make minimum payments, miss the promotional deadline, or start using the card for new purchases.

3. Personal Line of Credit

A personal line of credit gives flexible access to funds up to a set limit. You can borrow, repay, and borrow again. Rates may be lower than credit cards, but payments can change if the rate is variable.

A line of credit can be useful for disciplined borrowers. It can be risky if it becomes another revolving debt that never gets fully paid off.

If you’re also comparing ongoing borrowing options, learn more about our line of credit options or see our guide comparing a personal line of credit vs credit card.

4. HELOC or Home Equity Loan

Homeowners may be able to use home equity to consolidate debt. A home equity line of credit or home equity loan may offer a lower rate because the debt is secured against the home.

This can reduce interest costs, but it also increases risk. If you cannot repay, your home may be at risk. This option should be considered carefully, especially if you are turning unsecured debt into debt secured against your property.

5. Secured Consolidation Loan

A secured consolidation loan uses collateral, such as a vehicle or savings, to reduce lender risk. This may improve approval chances or lower the rate.

The risk is that you could lose the asset if you do not repay the loan.

6. Debt Management Plan

A debt management plan is usually arranged through a non-profit credit counselling agency. The agency may work with creditors to reduce or stop interest and create one monthly payment.

This is not the same as a loan. It may be better for borrowers who cannot qualify for affordable consolidation but can still repay their debts over time.

7. Consumer Proposal

A consumer proposal is a legal debt solution arranged through a Licensed Insolvency Trustee. It allows eligible borrowers to make an offer to repay part of what they owe over time.

This can reduce debt, but it affects credit and should only be considered after reviewing the consequences carefully.

8. Bankruptcy

Bankruptcy is a legal insolvency process for people who cannot repay their debts. It may discharge many unsecured debts, but it has serious credit and legal consequences.

Bankruptcy is not debt consolidation. It is usually considered when repayment is no longer realistic.

Debt Consolidation vs Other Debt Solutions

| Option | Best For | Main Risk |

|---|---|---|

| Debt consolidation loan | Borrowers with income and manageable debt | May cost more if term is too long |

| Balance transfer | Credit card debt paid off quickly | Promo rate may expire |

| Debt management plan | People needing creditor support | May affect credit access |

| Consumer proposal | People who cannot repay full debt | Serious credit impact |

| Bankruptcy | Severe insolvency | Major financial and credit consequences |

If you are unsure whether you need consolidation or a more formal debt solution, read our debt relief and consolidation Canada guide.

Canadian Debt Trends and Why Consolidation Matters

Many Canadians use credit cards, lines of credit, and personal loans to manage rising costs. When interest rates are high, carrying balances can become expensive quickly.

According to Statistics Canada, household debt remains high, with mortgages, credit cards, personal loans and lines of credit making up a significant share of consumer borrowing. When interest rates rise, minimum payments often increase and more of each payment goes toward interest instead of reducing the balance. For borrowers carrying several high-interest debts, this is one reason debt consolidation becomes worth exploring.

For official consumer guidance on managing debt, review the Financial Consumer Agency of Canada debt resources.

Common Debt Consolidation Mistakes

Choosing the lowest monthly payment only

A lower payment can help cash flow, but it may cost more if the repayment term is much longer. Always compare the total repayment amount.

Ignoring fees

Some loans include administration fees, insurance costs, or penalties. These can reduce or eliminate savings.

Using credit cards after consolidation

This is one of the biggest risks. If you consolidate credit cards and then use them again, you may end up with more debt than before.

Borrowing more than needed

Only borrow what is required to pay off the debts you plan to consolidate. Extra borrowing increases interest and repayment pressure.

Not fixing the budget problem

Consolidation can simplify debt, but it does not fix overspending or income shortfalls. A realistic budget is still needed.

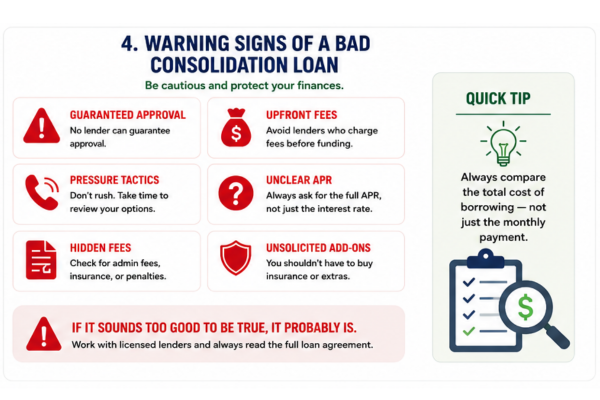

Warning Signs of a Bad Debt Consolidation Loan

Be careful if a lender:

- Promises guaranteed approval.

- Asks for upfront fees before funding.

- Does not clearly show the APR.

- Pressures you to sign quickly.

- Refuses to provide a written loan agreement.

- Adds insurance or fees you did not request.

- Will not explain the total cost of borrowing.

A legitimate lender should clearly explain the loan amount, APR, repayment term, fees, payment schedule, and total cost before you accept.

How FatCat Loans Helps With Debt Consolidation

FatCat Loans helps Canadians compare loan options from participating lenders. We are not a lender and do not provide debt counselling or insolvency advice.

Through one online application, you may be able to compare loan options based on your income, credit profile, and borrowing needs. This can help you review available rates, repayment terms, and loan amounts before choosing an offer.

If you are ready to compare options, visit our debt consolidation loans Canada page or use our secure online application.

Frequently Asked Questions

What is debt consolidation in Canada?

Debt consolidation means combining several debts into one new payment. This is often done with a personal loan, balance transfer, line of credit, or other consolidation product.

Does debt consolidation reduce debt?

No. Debt consolidation does not erase debt. It reorganizes debt into one payment. You still repay what you owe unless you use a formal debt relief option such as a consumer proposal.

When does debt consolidation save money?

Debt consolidation may save money when the new loan has a lower APR than your current debts and the repayment term is not too long. Always compare the total cost of borrowing before accepting an offer.

Can I get debt consolidation with bad credit?

Possibly. Some lenders consider borrowers with lower credit scores, but rates may be higher. Approval depends on income, affordability, credit history, debt level, and lender criteria.

Will debt consolidation hurt my credit score?

Applying for a loan may cause a small temporary dip if there is a hard credit check. Over time, on-time payments and lower credit card balances may help your credit profile.

Is debt consolidation better than a consumer proposal?

It depends on your situation. Debt consolidation may be better if you can repay your debts in full with a more affordable structure. A consumer proposal may be considered if you cannot repay the full amount owed.

What debts can I consolidate?

Common debts include credit cards, store cards, personal loans, lines of credit, and installment loans. Secured debts, student loans, tax debts, or support payments may be harder to consolidate.

What is the biggest risk of debt consolidation?

The biggest risk is creating new debt after consolidating old debt. If you keep using credit cards, you may end up with both the consolidation loan and new credit card balances.

Final Thoughts

For Canadians overwhelmed by multiple payments, high interest, and financial stress, debt consolidation can be a strategic way to regain control. By merging debts into one affordable monthly payment — and committing to responsible repayment — borrowers can simplify their finances and work toward long-term financial stability.

Ready to Compare Debt Consolidation Loans?

At FatCat Loans, you can compare loan offers from trusted Canadian lenders through one simple application. Compare interest rates, repayment terms, and loan amounts to find an option that fits your budget, with no obligation to accept an offer.

✅ Tailored solutions for Canadian borrowers

✅ Simple and transparent loan-matching process

✅ Supportive guidance every step of the way

Compare debt consolidation loan offers today.

Remember: Debt consolidation works best when it forms part of a realistic repayment plan. Before accepting any loan, compare the APR, repayment term, fees, and total cost of borrowing, and make sure the monthly payment fits comfortably within your budget.

Disclosure: This article is for informational purposes only and does not constitute financial advice. Loan terms, rates, and eligibility vary by lender and province. FatCat Loans is a loan comparison platform, not a lender. Always review lender agreements carefully before accepting a loan.

The FatCat Loans Editorial Team delivers clear, accurate, and unbiased guidance on loans, credit, and personal finance in Canada. Our writers follow strict editorial standards to ensure every article is trustworthy, well-researched, and easy to understand, helping readers make confident financial decisions.