Personal Loans Canada: Compare Loan Options Up to $50,000

Personal loans in Canada are lump-sum borrowing products available for almost any purpose - debt consolidation, home repairs, medical bills, moving costs, or unexpected expenses. FatCat Loans is a Canadian loan-matching service that connects you with licensed lenders in our network, including Spring Financial, easyfinancial, Magical Credit, and others. One application lets you compare offers side by side with no obligation to accept.

Loan amounts typically range from $500 to $50,000. Most applicants receive a decision within minutes, and funds are typically sent by e-transfer within the same business day or by the next business day after approval.

What Can You Use a Personal Loan for in Canada?

Personal loans are flexible - lenders generally do not restrict how you use the funds. However, the reason you are borrowing does affect which product and loan term makes the most sense. Here are the most common uses:

- Debt consolidation: Combining multiple credit card or loan payments into one fixed monthly payment, often at a lower rate than the debts being replaced. Compare the total repayment cost of the personal loan against your current combined payments before proceeding.

- Home repairs or renovations: A defined project cost makes a personal loan a good fit - you borrow the amount you need and repay over a fixed term.

- Emergency expenses: Unexpected bills, car repairs, or medical costs. The ability to receive funds by e-transfer the same or next business day makes personal loans practical for time-sensitive needs.

- Major purchases: Appliances, furniture, or other one-time costs where paying in installments is more manageable than paying upfront or using a high-interest credit card.

- Moving costs: First and last month's rent, deposits, and relocation expenses.

If your primary goal is to reduce the total interest you are paying across multiple debts, also compare our debt consolidation loans page before deciding.

Why Borrowers Compare Personal Loan Options

- Fast online process: Complete the application in minutes and review offers before accepting.

- Options for different credit profiles: Many lenders consider income, affordability, and overall financial stability in addition to credit history.

- Flexible amounts and terms: Personal loans are available in a range of amounts and repayment terms depending on your financial profile.

- Unsecured options available: Many personal loans do not require collateral.

- Transparent comparison: Review rates, repayment schedules, fees, and total borrowing cost before accepting any offer.

Comparing multiple personal loan offers in one place can help you find a loan structure that better fits your budget and borrowing needs.

Why Canadians Compare Personal Loans Before Applying

Not all personal loans are the same. Two lenders may offer very different borrowing amounts, repayment schedules, fees, and annual percentage rates for the same applicant. Comparing lenders first can help you avoid overpaying and find a loan structure that better matches your monthly budget.

For example, some borrowers prioritize lower monthly payments over a shorter term, while others want to repay quickly to reduce total borrowing costs. If you have fair or bad credit, comparing options becomes even more important because rates and conditions can vary significantly between lenders.

By reviewing multiple personal loan options in one place, Canadians can make a more informed borrowing decision instead of choosing the first offer they see.

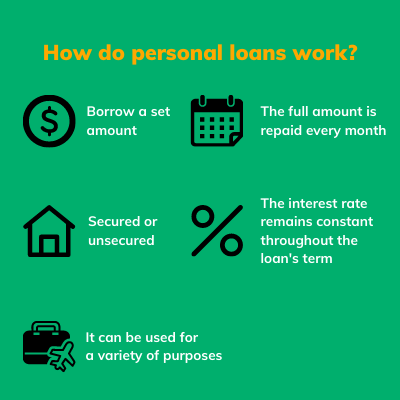

What Are Personal Loans?

Personal loans are borrowing options that provide a lump sum of money for many common personal expenses. Unlike specific loans such as car loans or mortgages, personal loans in Canada can be used for debt consolidation, home improvements, medical bills, vacations, or emergencies. They are often unsecured, meaning collateral is not usually required, and many are offered with structured repayment terms.

Personal loans are commonly offered with repayment terms ranging from about 3 to 60 months, although available terms depend on the lender and your financial profile.

Interest rates for personal loans in Canada are based on your credit profile, income, existing debt obligations, loan amount, and repayment term. Borrowers with stronger credit and affordability usually qualify for lower rates, while higher-risk applications often carry higher borrowing costs.

If you're exploring borrowing options, compare lenders and rates in our personal loan comparison guide.

How to Apply for Personal Loans in Canada

Applying for instant personal loans at FatCat Loans is easy and takes just a few minutes:

- Fill Out the Online Form: Provide basic details like your income, employment, and desired loan amount on our secure application page.

- Receive Matched Offers: Based on your application, you’ll be presented with personal loan options you may qualify for.

- Review and Accept: Receive offers with clear terms, including interest rates and repayment schedules.

- Receive Your Funds: Once approved, funds are typically sent within the same day or next business day after documents are signed.

No in-person visits required. Start your application here: Apply Now.

For other borrowing needs, check out our online loans or car loans.

What Income Types Qualify for a Personal Loan in Canada?

Personal loan lenders in our network assess affordability based on your income source and stability. You do not need to be traditionally employed to qualify. Accepted income types typically include:

- Employment income: Full-time or part-time, paid via direct deposit

- Self-employment income: Accepted by some lenders with recent bank statements as proof

- Employment Insurance (EI): Accepted as qualifying income by most lenders

- Canada Pension Plan (CPP) or Old Age Security (OAS): Accepted for retirement-age applicants

- Private pension income: Employer-sponsored or personal pension payments

- Ontario Disability Support Program (ODSP): Accepted by several lenders in our network

- Canada Child Benefit (CCB): May be counted alongside other income sources

In most cases, income must be deposited into an active Canadian bank account. Lenders may ask for recent bank statements or benefit confirmation letters to verify income stability.

Note: Not every lender in our network accepts every income type. You will see each lender's specific requirements before accepting any offer.

What Lenders Usually Look At When Reviewing a Personal Loan Application

While every lender has its own criteria, most providers look at a combination of income, employment stability, existing debt obligations, banking history, requested loan amount, and sometimes credit history. A higher income or lower debt load may improve your chances of approval or help you qualify for better terms.

Many lenders focus more heavily on affordability than on credit score alone. This can help borrowers with imperfect credit qualify, although higher-risk applications often come with higher borrowing costs.

Before applying, it can help to have the following ready:

- Government-issued ID

- Proof of income or recent bank statements

- Your banking information

- Your employer details, if applicable

- A clear idea of how much you need to borrow and what monthly payment you can realistically afford

What Do You Need to Qualify for a Personal Loan in Canada?

To qualify for personal loans online in Canada, you typically need to meet these basic criteria:

- Be a Canadian resident aged 18 or older.

- Have a steady source of income (employment, pension, or benefits).

- Possess an active Canadian bank account.

- Provide proof of identity and address.

Most lenders perform a soft credit check to verify identity and review your credit profile. Borrowers with stronger credit usually qualify for better rates and larger amounts, but many lenders also consider income and affordability when reviewing applications. If your credit is a concern, you can also compare options on our bad credit loans Canada page.

What Interest Rates Apply to Personal Loans in Canada?

Personal loan rates in Canada vary by lender, credit score, income, and loan term. The table below shows typical APR ranges based on credit tier to help you understand what rate is realistic before applying.

| Credit Score | Tier | Typical APR | Lender Type |

|---|---|---|---|

| 760–900 | Excellent | 9.99%–14.99% | Banks, credit unions, prime online lenders |

| 660–759 | Good | 14.99%–24.99% | Online lenders, some credit unions |

| 560–659 | Fair | 24.99%–32.99% | Alternative / near-prime lenders |

| 300–559 | Poor | 29.99%–35% | High-approval alternative lenders |

Maximum rate in Canada: 35% APR for most consumer loans (Criminal Code s.347, effective January 2025).

What Does a Personal Loan Actually Cost?

To understand the true cost, here are three representative examples:

- Good credit (score ~710, $10,000 over 36 months at 16.99% APR): Monthly payment approx. $355. Total interest approx. $2,780. Total repaid approx. $12,780.

- Fair credit (score ~610, $5,000 over 36 months at 29.99% APR): Monthly payment approx. $210. Total interest approx. $2,570. Total repaid approx. $7,570.

- Poor credit (score ~520, $3,000 over 24 months at 34.99% APR): Monthly payment approx. $163. Total interest approx. $912. Total repaid approx. $3,912.

These examples are illustrative. Your actual rate and terms depend on your lender, credit profile, income, and loan term. Use our cost of borrowing calculator to estimate your own repayment scenario.

Example: What a Personal Loan May Cost

Before accepting a personal loan, review the full cost of borrowing — not just the monthly payment. A lower monthly payment can still cost more overall if the repayment term is extended.

- Loan amount: $8,000

- APR: 24.99%

- Term: 36 months

- Estimated monthly payment: about $315–$325

- Total repayment: about $11,300–$11,700

- Total cost of borrowing: about $3,300–$3,700

This example shows why comparing APR, fees, repayment term, and total repayment amount matters before accepting an offer.

Personal loan rates in Canada are based on your credit profile, income, existing debt obligations, loan amount, and repayment term. Many personal loans fall within a range of about 9.99% to 35% APR, although higher-risk borrowing products may cost more depending on structure and lender criteria.

Factors influencing your rate include:

- Credit history

- Income and employment stability

- Loan amount and term

There are no fees to use this service. Always review your lender’s agreement carefully for full details on rates, fees, repayment terms, and total borrowing cost.

If high-interest debt is your main concern, consider consolidation loans Canada as an alternative.

For official consumer borrowing guidance, visit the Government of Canada — FCAC Loan Resource.

Canadian borrowers have the right to clear disclosure of interest rates, fees, repayment terms, and the total cost of borrowing before accepting a personal loan. Reviewing the full loan agreement is important so you understand exactly how interest, fees, and missed-payment charges are applied.

Depending on your province, lenders may also be overseen by provincial regulators such as FSRA in Ontario, BCFSA in British Columbia, and AMF in Quebec.

Important Things to Check Before Accepting a Personal Loan

Before signing a loan agreement, take a few minutes to review the full cost of borrowing. The advertised rate is only one part of the picture. You should also confirm the repayment frequency, total repayment amount, any lender fees, and whether there are penalties or charges for missed payments.

It is also worth checking whether the loan is open or closed, whether you can repay early without penalty, and whether the lender reports payments to a credit bureau. For some borrowers, on-time payments may help build credit, while late payments can negatively affect it.

If the monthly payment feels difficult to manage, consider reducing the amount you borrow, extending the term carefully, or exploring alternatives such as a lower-cost line of credit, a consolidation loan, or speaking with a financial professional about your options.

Responsible borrowing starts with choosing a loan you can comfortably repay, not simply the largest amount available.

Personal Loans vs. Other Options

Wondering if a personal loan is right for you? Compare it to alternatives:

| Feature | Personal Loans | Payday Loans | Credit Cards |

|---|---|---|---|

| Loan Amount | $500 - $50,000 | Up to $1,500 | Varies by limit |

| Repayment Term | 3–60 months | 14–30 days | Revolving |

| Interest Rates | 9.99% - 35% APR | Provincial fee caps apply ($14–$17 per $100 borrowed) | 15–30% APR |

| Best For | Debt consolidation, large expenses | Short-term emergencies | Everyday purchases |

For advice on how to manage your loan, check out our responsible borrowing in Canada guide.

Learn more about how short-term loans work in our latest article.

Who Personal Loans May Be Best Suited For

Personal loans can make sense for Canadians who need a fixed amount of money and want predictable repayments over time. They are often used for debt consolidation, emergency expenses, home repairs, moving costs, medical bills, or other one-time purchases where paying in installments is more manageable than using a high-interest credit card.

They may be less suitable for ongoing day-to-day spending or situations where repayment would strain your budget. If you are already struggling with existing debt, it is important to compare the total borrowing cost carefully and consider whether a consolidation-focused option may be a better fit.

If you are unsure where to start, comparing personal loans alongside consolidation loans, lines of credit, and no credit check loans can help you choose a product that better matches your situation.

Frequently Asked Questions About Personal Loans in Canada

What is the maximum amount I can borrow with a personal loan in Canada?

Through FatCat Loans, loan amounts typically range from $500 to $50,000. The amount you qualify for depends on your income, existing debt obligations, and the lender's criteria. Higher amounts generally require stronger income documentation and a lower debt-to-income ratio.

Can I get a personal loan with bad credit in Canada?

Yes. Several lenders in our network approve borrowers with credit scores below 600 by assessing income, banking stability, and affordability rather than credit score alone. Rates are typically higher for lower credit profiles. See our bad credit loans page for dedicated options.

How quickly can I receive personal loan funds in Canada?

Most lenders in our network fund approved applications by e-transfer. For applications approved before 2pm EST on a business day, funds typically arrive the same day or by the next business day. Timing may vary depending on your lender and bank.

Will comparing personal loan options affect my credit score?

Applying through FatCat Loans involves a soft credit check, which does not affect your credit score. If you accept a loan offer, the lender may run a hard inquiry, which can temporarily reduce your score by a few points.

Can I repay a personal loan early in Canada?

Some personal loans allow early repayment without penalty. Others include prepayment conditions. Always review the loan agreement before accepting - specifically look for any prepayment clauses in the terms.

What can I use a personal loan for in Canada?

Most personal loans are unsecured and can be used for any legal purpose - debt consolidation, home repairs, medical bills, moving costs, major purchases, or emergency expenses. Confirm acceptable uses with the lender before accepting an offer.

What is the maximum interest rate on a personal loan in Canada?

As of January 1, 2025, the criminal interest rate threshold for most consumer loans in Canada is 35% APR (Criminal Code s.347). Lenders cannot legally charge above this rate on most personal installment loan products.

Do I need collateral for a personal loan?

Most personal loans available through FatCat Loans are unsecured, meaning no collateral is required. Secured personal loans, which use an asset as collateral, may offer lower rates but are less commonly available through online lenders.

What is a co-signer and does it help with a personal loan?

A co-signer is someone who agrees to be legally responsible for the loan if you cannot repay it. Adding a co-signer with stronger credit or higher income can improve your approval chances or help you qualify for a lower rate. Both parties share full responsibility for the debt, so this decision should be made carefully.

What if I am declined for a personal loan?

A decline does not mean no options are available. Consider: applying for a smaller amount, improving your debt-to-income ratio, adding a co-signer, or reviewing alternatives such as a line of credit, bad credit loan, or no credit check loan. Comparing options can help you find a product that better matches your current financial profile.

How do I know whether a personal loan payment is affordable?

A useful rule of thumb: your total monthly debt payments - including the new loan - should not exceed 40% of your gross monthly income. Before applying, compare the monthly payment, total repayment amount, and term length alongside your existing obligations.

Ready to compare your options? Apply online to review personal loan offers that match your borrowing needs and budget.

Soft check only*. Takes 2 Minutes.

FatCatLoans.ca is a Canadian loan-matching service, not a lender or financial advisor. We connect applicants with licensed lenders in our network and may receive a commission from lenders when a loan is funded. There is no cost to use our service.

Information on this website is intended to help Canadians understand borrowing options and does not constitute financial advice. Always review the lender's rates, fees, repayment terms, and total cost of borrowing before accepting any offer.

Loan matching services in Canada operate under applicable federal and provincial consumer protection laws. The Financial Consumer Agency of Canada (FCAC) provides guidance on borrower rights, while provincial regulators such as FSRA (Ontario), BCFSA (British Columbia), and AMF (Quebec) oversee lender licensing and compliance.