No Credit Check Loans Canada - Income-Based Approval

No credit check loans in Canada are borrowing options where lenders assess income, banking activity, and affordability rather than relying primarily on a traditional credit score. They are typically used for urgent expenses, short-term cash flow gaps, or situations where mainstream borrowing options are limited.

FatCat Loans is a Canadian loan-matching service that connects you with licensed lenders in our network, including Spring Financial, easyfinancial, Magical Credit, and others. One application lets you compare available options with no obligation to accept.

For short-term products, amounts typically range from $250 to $1,500. For longer-term instalment-style products, amounts up to $15,000 may be available depending on income and lender criteria. Most applicants receive a decision within minutes, with funds typically sent by e-transfer the same or next business day after approval.

How Quickly Can I Receive a No Credit Check Loan?

Lenders in our network fund approved applications via e-transfer. For most applicants with an e-transfer-enabled bank account, funds may arrive same-day or by the next business day after approval. Applying before 2pm EST on a business day gives you the best chance of same-day funding.

Funding speed depends on the lender, your application details, and your bank’s processing times. Some applications may take longer if extra verification is required or if the lender sends funds by direct deposit instead of e-transfer.

What affects your funding speed

- Time of day you apply: Applying before vs. after 2pm EST can affect whether funding is processed the same business day.

- Your bank: Some banks accept incoming e-transfers faster than others.

- Additional verification: Some lenders may request extra documents before releasing funds.

- Funding method: Direct deposit instead of e-transfer may take 1–2 business days depending on your bank.

How FatCat Loans Helps You Compare No Credit Check Loan Options

FatCat Loans helps you compare loan options from lenders that may place less emphasis on a traditional credit score.

“No credit check” does not mean no verification. Lenders still review your financial situation to determine whether a loan is appropriate, and approval is never guaranteed.

Before accepting any offer, take time to review the interest rate, repayment terms, and total borrowing cost to make sure the loan is suitable for your needs.

Benefits of No Credit Check Loans with FatCat Loans

- Fast online process: Applications are submitted online, many lenders provide quick decisions, and approved funds may arrive the same day or by the next business day depending on verification and bank processing.

- Alternative approval checks: Some lenders may focus more on income and affordability rather than a traditional hard credit inquiry.

- Accessible for Bad Credit: Options available for poor or limited credit.

- Flexible Loan Amounts: Borrow from $500 to $50,000.

- Transparent Matching: Connected to licensed lenders — no upfront fees.

You may also want to compare bad credit loans.

What Are No Credit Check Loans?

No credit check loans in Canada are borrowing options where lenders do not rely primarily on a traditional hard credit inquiry. Instead, approval decisions are often based on income, employment stability, and recent banking activity.

How No Credit Check Loan Approval Works

When a lender offers a no credit check loan, it usually means they are not relying mainly on a traditional hard credit inquiry to make the decision. Instead, they may focus more heavily on your current ability to repay.

- Income: Regular employment, pension, or benefits income may help support an application.

- Banking history: Lenders often review recent deposits, account activity, and signs of financial stability.

- Existing obligations: Your debt-to-income ratio and monthly commitments may affect eligibility.

- Requested loan amount: Applying for an amount that fits your income may improve affordability in the lender’s assessment.

This is why “no credit check” should never be treated as “no verification.” Legitimate lenders still need to verify identity, affordability, and the details on your application before funding a loan.

If you are comparing options, it may also help to review bad credit loans, personal loans, or online loans depending on the amount you need and how quickly you plan to repay it.

How Quickly Can You Receive a No Credit Check Loan in Canada?

Funding speed is a key concern for borrowers searching for no credit check options, as most are dealing with urgent situations. Here is what to expect:

- Same-day e-transfer: Available from most lenders for applications approved before 2pm EST on a business day, provided your bank accepts incoming e-transfers automatically.

- Next business day: The most common outcome for applications approved later in the day or where document verification adds a small delay.

- 1–2 business days (direct deposit): Some lenders send funds via direct deposit rather than e-transfer, with timing depending on your bank.

If same-day funding is essential, apply as early in the business day as possible and have your income confirmation and banking details ready before starting the form.

What “No Credit Check” Really Means in Canada

Most borrowers searching for no credit check loans want to avoid a hard inquiry that could affect their credit score. In practice, many lenders use alternative approval criteria rather than relying solely on credit history.

Some lenders may still perform identity verification or limited checks as part of responsible lending. You will always be shown the lender’s full terms before accepting any loan offer.

If you’re researching how no credit check and limited bank verification loans work, including how they compare to payday loans and what risks to watch for, read our in-depth guide on how no credit check and no bank verification loans work in Canada.

How to Apply for No Credit Check Loans in Canada

- Complete the Online Form: Provide income and employment details securely.

- Receive Matched Offers: Based on your application, you’ll be shown loan options you may qualify for.

- Review Loan Terms: See rates, fees, and repayment schedules clearly.

- Receive Funds: Funding time depends on the lender and your bank.

Start your application here: Apply Now.

You may also explore personal loans or car loans.

What Income Types Are Accepted for No Credit Check Loans?

Lenders in our network typically accept a range of income sources, not just traditional employment. Approval is based on your overall ability to repay, which may include government benefits, pensions, or other consistent income.

Common income types that may be accepted include:

- Employment income: Full-time or part-time income paid through direct deposit

- Employment Insurance (EI): Temporary income support for eligible workers

- Canada Pension Plan (CPP) or Old Age Security (OAS): Retirement income

- Private pension income: Employer or individual pension plans

- Ontario Disability Support Program (ODSP): Disability-related income support

- Ontario Works (OW) or provincial assistance: Social assistance programs

- Canada Child Benefit (CCB) or Child Tax Benefit: Family-related government benefits

- Canada Workers Benefit (CWB): Income supplement for eligible workers

If you have a steady source of income — even if it’s not traditional employment — you may still be eligible to compare loan options.

In most cases, income must be received by direct deposit into an active Canadian bank account. Some lenders may also accept self-employment income if you can provide recent bank statements or proof of consistent deposits.

Important: Not all lenders accept every income type. Eligibility depends on the lender’s criteria, and you will be able to review specific requirements before accepting any loan offer.

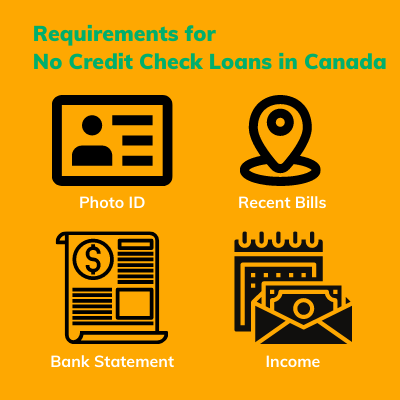

What Do No Credit Check Lenders Actually Assess?

Despite the name, no credit check lenders still verify your financial situation before approving a loan. They simply do not rely primarily on your credit history. Here is what they typically review instead:

- Income: You need a regular, verifiable income source - employment, pension, or benefits. The lender needs to confirm you can afford the repayment.

- Income stability: How long you have been receiving your income matters. Most lenders look for at least 3 months of consistent deposits.

- Banking history: Lenders review recent account activity. Frequent NSF charges, irregular deposits, or an account with very low average balances can reduce your options.

- Debt-to-income ratio: Your existing monthly obligations are assessed alongside your income. If a new loan payment would leave your budget too thin, some lenders will decline or offer a smaller amount.

- Identity verification: All legitimate lenders verify your identity - government ID and banking information are standard requirements.

You do not need a specific credit score to apply. The above factors determine whether a loan is approved, how much you can borrow, and at what cost.

What Income Types Are Accepted for No Credit Check Loans?

A large proportion of people searching for no credit check loans receive government benefits or non-traditional income. Most lenders in our network accept the following:

- Employment income: Full-time or part-time, paid via direct deposit

- Employment Insurance (EI): Accepted by most lenders as qualifying income

- Canada Pension Plan (CPP) or Old Age Security (OAS)

- Ontario Disability Support Program (ODSP)

- Ontario Works (OW) or equivalent provincial assistance

- Canada Child Benefit (CCB) or Child Tax Benefit

- Canada Workers Benefit (CWB)

- Private pension income

- Self-employment income: Accepted by some lenders with recent bank statements as proof

In most cases, income must be deposited into an active Canadian bank account. Some lenders may ask for a recent bank statement or benefit confirmation letter to verify that income is stable and ongoing.

Note: Not every lender accepts every income type. You will see each lender's specific eligibility requirements before accepting any offer.

When a No Credit Check Loan May Be a Good Option

A no credit check loan may be worth considering if you need funds for a specific purpose, have limited credit history or recent credit issues, and can comfortably manage the repayment within your current budget.

- Emergency expenses such as urgent repairs or unexpected bills

- Short-term cash flow gaps where repayment is realistic

- Situations where mainstream borrowing options are limited

When you may want to compare alternatives first

- If the loan payment would leave your budget too tight each month

- If you need repeated access to credit rather than a one-time lump sum

- If your main goal is to lower multiple debt payments through one structured product

In those cases, you may want to compare a line of credit, a debt consolidation loan, or a more structured installment loan. The right product depends on your repayment plan, not just whether approval is possible.

No Credit Check Loan Availability by Province

If you're searching for no credit check loans in Ontario, BC, Alberta, or other provinces, availability depends on local regulations and whether lenders are licensed to operate in your area.

No credit check loan availability, regulations, and maximum borrowing costs vary by province in Canada. Lenders must follow provincial consumer protection laws, and not all lenders operate nationwide. Below is a general overview of how regulations differ across major provinces.

FatCat Loans works with licensed lenders where available. Always confirm lender licensing, rates, and terms before accepting an offer.

Ontario

In Ontario, payday-style and short-term lenders are regulated by the Financial Services Regulatory Authority of Ontario (FSRA). The maximum cost of borrowing for payday loans is capped at $14 per $100 borrowed.

Lenders must hold a valid FSRA license to operate legally. You can explore options on our Ontario loans page.

British Columbia

In British Columbia, lenders are regulated by the BC Financial Services Authority (BCFSA). The maximum cost for payday loans is $14 per $100 borrowed, similar to Ontario.

Borrowers should ensure any lender is properly licensed. Learn more on our BC loans page.

Alberta

Alberta lenders operate under the Consumer Protection Act. The maximum borrowing cost for payday loans is $14 per $100 borrowed.

Lenders must follow provincial disclosure and licensing rules. See available options on our Alberta loans page.

Manitoba and Nova Scotia

Manitoba and Nova Scotia have slightly higher borrowing cost caps, typically up to $17 per $100 borrowed for payday-style loans.

These provinces also require lenders to be licensed and to clearly disclose all fees and repayment terms.

Saskatchewan

Saskatchewan also caps borrowing costs at approximately $17 per $100 borrowed for payday loans. Regulations are enforced at the provincial level, and lenders must meet licensing and disclosure requirements.

Quebec

Quebec has stricter consumer protection laws than other provinces, including lower allowable interest rates and tighter lending rules. As a result, many short-term and no credit check lenders do not operate in Quebec.

If you are located in Quebec, availability may be limited, and you should confirm whether a lender is authorized to operate in your province before applying.

All Other Provinces and Territories

In other provinces and territories, lenders must comply with local consumer protection legislation and licensing requirements. Borrowing costs, regulations, and lender availability may vary.

Important: No matter where you live, always verify that a lender is licensed in your province and review the total cost of borrowing before accepting a loan. You can also consult resources from the Financial Consumer Agency of Canada (FCAC) or your provincial regulator for additional guidance.

About “Guaranteed Approval” and “No Refusal” Loans

Searches for terms like “guaranteed approval” or “no refusal loans” are common, especially for borrowers with poor credit. However, no legitimate lender can guarantee approval for every applicant.

Some lenders offer higher-approval options by using flexible criteria focused on income and affordability. Loan approval, amounts, and rates still depend on meeting lender requirements.

Learn more in our guide: guaranteed approval loans Canada.

What Are the Risks of a No Credit Check Loan?

No credit check loans can be helpful in some situations, but they can also carry higher borrowing costs than standard loans. Before accepting any offer, it is important to review the total cost of borrowing, not just the speed of approval.

Example: What a No Credit Check Loan May Cost

Before accepting a no credit check loan, review the full cost of borrowing — not just the speed of approval. For example, a $2,000 loan at a higher APR over 12 months may have a manageable monthly payment but still cost significantly more overall than a lower-cost alternative.

- Higher APRs may apply: If a lender takes on more risk, the rate may be higher than on other loan products.

- Shorter repayment periods can increase pressure: A fast loan can still become expensive if the repayment window is tight.

- Late payments may trigger fees: Missed or late payments can increase the total cost and may affect your credit profile.

- Scam offers are common in this category: Be cautious of anyone asking for upfront deposits, gift cards, or unusual “insurance” or “processing” fees.

If you are unsure whether an offer is legitimate, review our fraud alert page before sharing personal information or sending any money. Legitimate lenders do not need upfront payments to “unlock” a loan.

What Does a No Credit Check Loan Cost in Canada?

No credit check loans generally carry higher rates than standard personal loans because lenders take on more risk by not relying on credit history. Costs vary by product type:

Short-term (payday-style) products

Provincial fee caps apply. Maximum allowable cost per $100 borrowed:

- Ontario, British Columbia, Alberta: $14 per $100

- Manitoba, Nova Scotia, Saskatchewan: $17 per $100

- New Brunswick, Newfoundland & Labrador: $14 per $100

Example: Borrow $500 in Ontario for 14 days at $14 per $100.

Total cost: $70. Total repayment: $570. Annualized APR: approximately 365%.

Longer-term instalment products (no hard credit check)

These products carry lower annualized rates but higher absolute interest due to the longer repayment period:

- Typical APR range: 29.99%–35%

- Maximum APR in Canada: 35% (Criminal Code s.347, effective January 2025)

Example: Borrow $2,000 at 34.99% APR over 18 months.

Monthly payment: approx. $138. Total interest: approx. $484. Total repaid: approx. $2,484.

Always review the full repayment amount - not just the monthly payment - before accepting any loan offer.

No Credit Check Loans vs Other Borrowing Options

No credit check loans are only one type of borrowing option. Depending on your financial situation, another product may be a better fit.

- Bad Credit Loans: Often suitable for borrowers with lower credit scores who still want structured repayment terms.

- Personal Loans: May offer better rates for borrowers who qualify and need a lump sum for a defined purpose.

- Lines of Credit: May be more flexible for repeated borrowing, though they require discipline to manage well.

- Debt Consolidation Loans: Better suited when the goal is to combine and simplify multiple existing payments.

How to Borrow More Safely

Before taking any loan, ask yourself a few simple questions:

- Can I comfortably afford the payment after rent, groceries, utilities, and current debt payments?

- Do I understand the APR, repayment schedule, and total repayment amount?

- Am I borrowing for a one-time need, or am I trying to cover an ongoing budget problem?

If the loan does not clearly fit your budget, consider borrowing a smaller amount or comparing other products first. Responsible borrowing means choosing a loan you can repay without needing to borrow again immediately.

Frequently Asked Questions About No Credit Check Loans in Canada

Do no credit check loans actually exist in Canada?

Yes. Many alternative lenders offer products where the decision is based primarily on income and banking activity rather than a traditional credit score check. However, all legitimate lenders still verify identity and affordability - "no credit check" means no hard credit inquiry, not no verification at all.

What is the maximum interest rate on a no credit check loan in Canada?

For most consumer instalment loans in Canada, the maximum rate is 35% APR (Criminal Code s.347, effective January 2025). For short-term payday-style products, provincial fee caps apply instead - typically $14–$17 per $100 borrowed depending on the province.

Can I get a no credit check loan if I receive EI or government benefits?

Yes. Most lenders in our network accept EI, ODSP, Ontario Works, CPP, OAS, and Canada Child Benefit as qualifying income, provided it is paid by direct deposit into an active Canadian bank account.

How quickly can I receive a no credit check loan in Canada?

Most lenders fund approved applications by e-transfer. For applications approved before 2pm EST on a business day, funds typically arrive the same day. Applications approved later typically fund by the next business day.

Are no credit check loans the same as payday loans?

Not always. Payday loans are a specific type of short-term product with a lump-sum repayment due on your next payday. No credit check loans can also include longer-term instalment products with monthly payments over 3–24 months. The two differ in structure, term, and cost.

Can I get a no credit check loan with a bankruptcy or consumer proposal on my record?

In many cases yes, depending on your current income and how long ago the event occurred. Some lenders in our network work specifically with borrowers who have had past credit events.

Will applying affect my credit score?

Applying through FatCat Loans involves a soft check, which does not affect your score. If you accept an offer, the lender may run a hard inquiry, which can temporarily reduce your score by a few points. Some lenders use alternative verification only - this will be disclosed in the lender's terms.

Are no credit check loans more expensive than regular personal loans?

Generally yes. Because lenders take on more risk by not relying on credit history, rates are typically higher. Short-term products carry the highest annualized cost. Always review the full repayment amount before accepting - not just the monthly payment.

Can I get a no credit check loan in Quebec?

Quebec has stricter consumer lending laws than other provinces. Some short-term lenders in our network do not operate in Quebec, or may offer fewer products there. Confirm lender availability for Quebec before applying.

What happens if I cannot repay a no credit check loan?

Missing a payment typically results in a late fee and may affect your credit report. Contact your lender before the due date if you anticipate difficulty - many will offer a deferral or modified schedule rather than proceed directly to collections.

Is it safe to apply for a no credit check loan online in Canada?

It is safe when applying through a reputable, licensed provider. Avoid any lender that requests upfront fees before funding, guarantees approval without reviewing your application, or asks for payment via gift card or wire transfer. Visit our fraud alert page for a full checklist of warning signs.

Soft check only. Takes 2 Minutes.

FatCatLoans.ca is a Canadian loan-matching service, not a lender or financial advisor. We connect applicants with licensed lenders in our network and may receive a commission from lenders when a loan is funded. There is no cost to use our service.

Information on this website is intended to help Canadians understand borrowing options and does not constitute financial advice. Always review the lender's rates, fees, repayment terms, and total cost of borrowing before accepting any offer.

Loan matching services in Canada operate under applicable federal and provincial consumer protection laws. The Financial Consumer Agency of Canada (FCAC) provides guidance on borrower rights, while provincial regulators such as FSRA (Ontario), BCFSA (British Columbia), and AMF (Quebec) oversee lender licensing and compliance.