What Is LoanConnect and How Does It Work?

Last Updated: July 2026

LoanConnect is a Canadian online loan comparison platform that connects borrowers with a network of participating lenders. Unlike a direct lender, LoanConnect does not issue loans itself. Instead, it allows borrowers to complete a single online application that may be matched with lenders offering personal loans and other credit products.

In this review, we’ll explain how LoanConnect works, who it may be suitable for, the types of loans available through its lending network, its advantages and drawbacks, and how it compares with FatCat Loans and other Canadian loan comparison services.

Quick Answer

LoanConnect is not a direct lender. Instead, it matches eligible borrowers with lenders that may offer personal loans and other credit products. Before accepting any loan offer, compare the Annual Percentage Rate (APR), fees, repayment schedule and total borrowing cost with other Canadian loan comparison platforms and lenders.

Important: FatCat Loans is a loan comparison platform, not a direct lender. Loan approval, interest rates and repayment terms are determined by the participating lender that reviews your application.

LoanConnect at a Glance

This summary provides a quick overview of LoanConnect before exploring the platform in more detail below.

| Feature | Details |

|---|---|

| Company Type | Canadian loan comparison platform |

| Application | Online |

| Direct Lender | No |

| Loan Products | Varies by participating lender |

| Funding | Provided by the approved lender |

| Availability | Canada (subject to participating lenders) |

| Best For | Borrowers wanting to compare multiple lending options through one application |

Table of Contents

- What Is LoanConnect and How Does It Work?

- LoanConnect at a Glance

- How LoanConnect Fits Into Canada’s Lending Landscape

- How Does LoanConnect Compare With Traditional Banks?

- Loan Types Available Through LoanConnect

- Eligibility & Application Process

- Interest Rates, Fees & Repayment

- What Should You Check Before Accepting a Loan Offer?

- Advantages

- Potential Drawbacks

- Who Should Consider LoanConnect?

- LoanConnect vs FatCat Loans

- Customer Reviews

- Is LoanConnect Legit?

- Alternatives

- Is LoanConnect Right for You?

- How We Review Loan Comparison Platforms

- Frequently Asked Questions

- Final Verdict

How LoanConnect Fits Into Canada’s Lending Landscape

Canada’s lending market includes traditional banks, credit unions, online lenders in Canada and loan comparison platforms. Unlike direct lenders that provide their own loan products, comparison platforms help borrowers submit a single application that can be assessed by multiple lending partners.

LoanConnect operates as a loan matching service. Rather than making lending decisions itself, it connects eligible borrowers with lenders that may offer personal loans or other credit products, depending on the applicant’s financial circumstances and the participating lender’s eligibility criteria.

For borrowers who want to compare multiple lenders without completing several separate applications, loan comparison platforms can provide a convenient starting point. However, it’s still important to compare the APR, repayment terms, fees and total borrowing cost before accepting any loan offer.

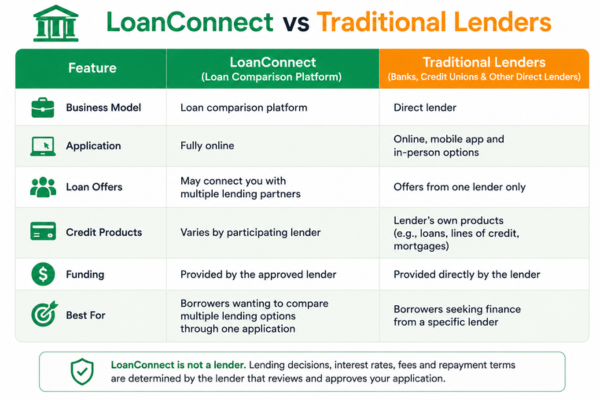

How Does LoanConnect Compare With Traditional Banks?

| Feature | LoanConnect | Traditional Banks |

|---|---|---|

| Business Model | Loan comparison platform | Direct lender |

| Application | Fully online | Online and branch options |

| Loan Offers | May connect borrowers with multiple lending partners | Bank’s own lending products |

| Credit Products | Varies by participating lender | Personal loans, lines of credit and other banking products |

| Funding | Provided by the participating lender if approved | Provided directly by the bank |

| Best For | Borrowers wanting to compare multiple lending options through one application | Borrowers seeking finance directly from their bank |

Unlike traditional banks, LoanConnect does not lend money directly. Instead, it helps eligible borrowers compare loan options from participating lenders, potentially reducing the need to submit multiple separate loan applications.

Because lending decisions are made by the individual lenders within LoanConnect’s network, available loan amounts, repayment terms, interest rates and eligibility requirements vary depending on the lender you are matched with.

As with any loan comparison platform, reviewing each loan offer carefully before accepting is essential. Comparing the total borrowing cost—not just the monthly repayment—can help you determine which option best fits your financial circumstances.

Loan Types Available Through LoanConnect

LoanConnect is not a lender, so it does not offer its own loan products. Instead, it connects eligible borrowers with lending partners that may provide a range of credit products depending on the applicant’s financial circumstances and the lender’s approval criteria.

The products available through LoanConnect’s lending network may vary over time and are determined by the participating lenders rather than LoanConnect itself.

Personal Loans

Many borrowers use LoanConnect to search for personal loans that can be used for a wide range of purposes, including unexpected expenses, home improvements, vehicle repairs, debt consolidation and other personal financial needs.

If you’d like to compare more borrowing options, our guide to personal loans in Canada explains how different lenders, loan amounts and repayment terms compare.

Installment Loans

Many lenders within LoanConnect’s network offer installment loans. These loans are repaid through fixed scheduled payments over an agreed loan term, making repayments easier for many borrowers to budget.

Unlike revolving credit, installment loans have a defined repayment period and are typically repaid until the balance has been cleared.

Our guide to installment loans in Canada explains how these loans work in more detail.

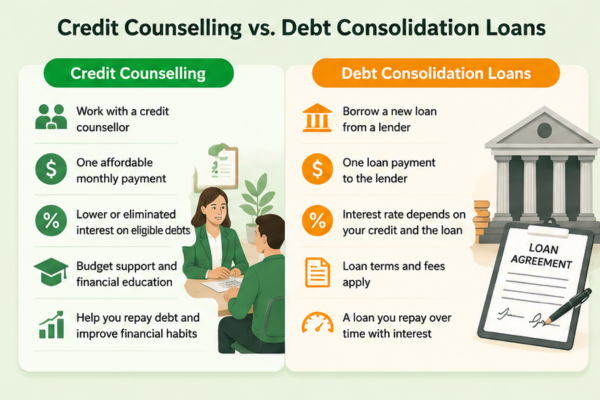

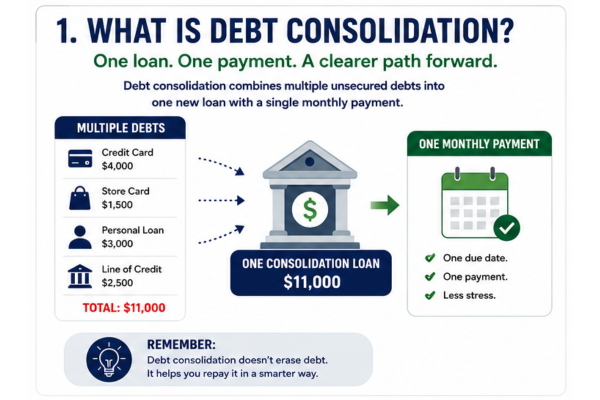

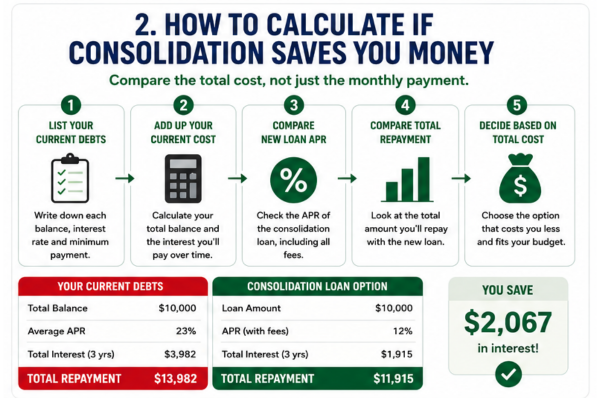

Debt Consolidation Loans

Some participating lenders may offer loans that borrowers use to consolidate existing debts into a single monthly repayment. Whether this option is available depends on the lender’s products and your individual financial circumstances.

Before consolidating debt, compare the total borrowing cost, repayment term and any applicable fees to determine whether consolidation is suitable for your situation. Our guide to debt consolidation loans in Canada explains when consolidation may be appropriate.

Bad Credit Loan Options

Some lenders within LoanConnect’s network may consider applicants with less-than-perfect credit histories. However, approval is never guaranteed and lenders may also consider factors such as income, affordability, existing debt obligations and employment status.

If your credit history is less than ideal, our guide to bad credit loans in Canada explains what lenders typically assess before making a lending decision.

If you’re working on rebuilding your credit profile before applying, read our guide on how to improve your credit score in Canada.

Eligibility & Application Process

LoanConnect aims to simplify the borrowing process by allowing applicants to complete a single online application that may be shared with participating lending partners. Individual lenders remain responsible for assessing each application and making lending decisions.

Although requirements vary by lender, applicants may typically be asked to provide:

- Proof of identity.

- Proof of Canadian residency.

- Employment and income information.

- An active Canadian bank account.

- Additional supporting documents if requested by the lender.

Depending on the lender reviewing your application, additional verification may be required before a final lending decision is made.

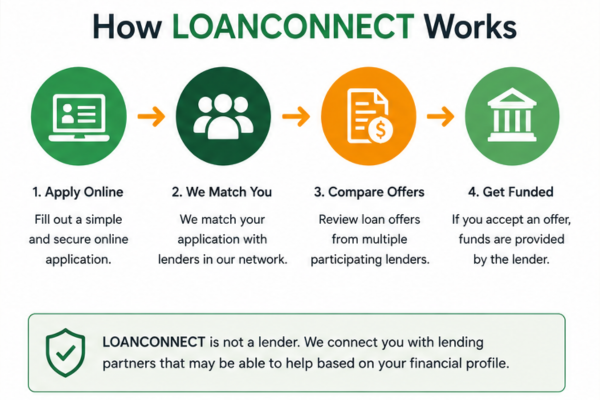

How the Application Process Works

- Complete LoanConnect’s secure online application.

- Provide your personal, employment and financial information.

- Your application is reviewed and may be matched with participating lenders.

- If matched, review any available loan offers carefully.

- If you accept an offer, the lender completes its verification and funding process.

Submitting an application through LoanConnect does not guarantee that you will receive a loan offer. Lending decisions remain subject to each participating lender’s affordability assessment, eligibility criteria and approval process.

Interest Rates, Fees & Repayment

Because LoanConnect is a loan comparison platform rather than a lender, it does not set interest rates or repayment terms. These are determined by the individual lender that reviews and approves your application.

Your loan offer may depend on several factors, including:

- Your credit profile.

- Your verified income.

- Your employment status.

- Your affordability assessment.

- Your existing debt obligations.

- The lender’s own approval criteria.

Before accepting any loan offer, carefully review:

- The Annual Percentage Rate (APR).

- Any origination, administration or NSF fees.

- Your repayment schedule.

- The total amount repayable over the loan term.

- Whether early repayment is permitted and whether any charges apply.

Understanding the total borrowing cost—not just the monthly repayment—can help you choose a loan that fits comfortably within your budget. You can estimate repayments using our loan calculator.

Depending on your borrowing needs, you may also wish to compare a line of credit with a personal loan before applying.

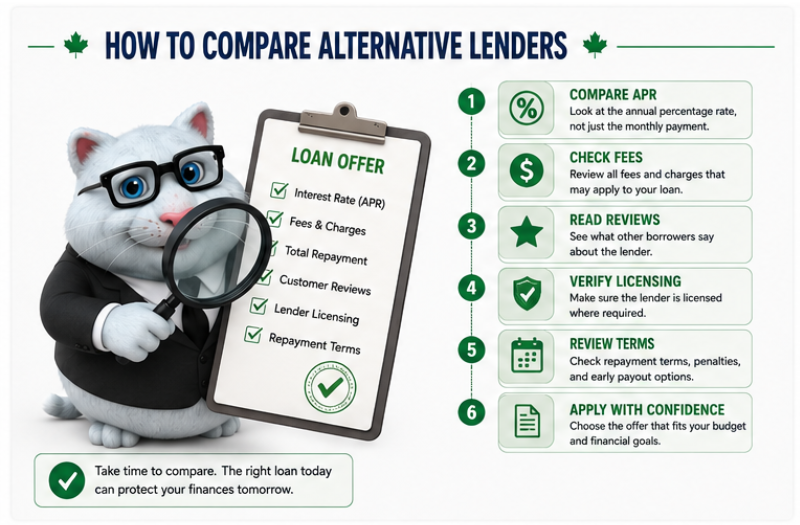

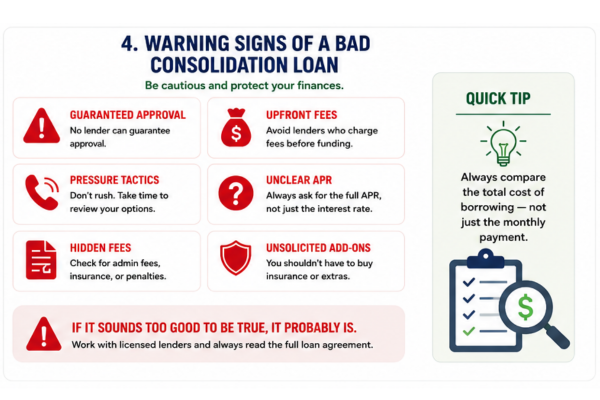

What Should You Check Before Accepting a Loan Offer?

Receiving a loan offer is only one part of the borrowing process. Before accepting any offer from a participating lender, compare the overall cost of borrowing rather than focusing solely on the monthly payment.

- Compare the Annual Percentage Rate (APR).

- Review all applicable fees.

- Understand the repayment schedule.

- Confirm the total amount repayable.

- Check whether early repayment is allowed without additional charges.

- Ensure the repayments fit comfortably within your monthly budget.

If you’re comparing offers from several lenders, understanding how credit enquiries work can also be helpful. Our guide to soft vs hard credit checks in Canada explains when different types of credit enquiries may affect your credit profile.

Advantages of Using LoanConnect

LoanConnect is designed to make it easier for borrowers to compare lending options through a single online application. Depending on your financial circumstances and borrowing needs, the following features may appeal to some applicants.

One Online Application

Rather than completing separate applications with multiple lenders, LoanConnect allows eligible borrowers to submit one application that may be matched with participating lending partners.

Access to Multiple Lending Partners

Because LoanConnect works with a network of lenders, borrowers may receive loan offers from lenders they may not have considered applying to individually. Available lenders and products vary over time.

Fully Online Process

The application process is completed online, allowing borrowers to compare potential lending options without visiting a physical branch.

Wide Range of Credit Profiles Considered

Participating lenders may consider applicants with a range of credit profiles. However, approval depends on each lender’s individual lending criteria, affordability assessment and verification process.

Potential Drawbacks

While LoanConnect may be suitable for many borrowers, it is not the right solution for everyone.

- LoanConnect does not make lending decisions or issue loans directly.

- Not every applicant will be matched with a lender.

- Interest rates, loan amounts and repayment terms vary depending on the participating lender.

- Borrowers should compare each loan offer carefully before accepting.

- Product availability and participating lenders may change over time.

As with any borrowing decision, comparing several lenders and loan comparison platforms can help you find a loan that best suits your financial circumstances.

Who Should Consider LoanConnect?

LoanConnect may be suitable for borrowers who:

- Want to compare multiple lenders through one online application.

- Prefer comparing loan offers before making a decision.

- Are looking for unsecured personal loan options.

- Don’t already have a preferred lender.

LoanConnect vs FatCat Loans

LoanConnect and FatCat Loans are both online loan comparison platforms rather than direct lenders. Instead of lending money themselves, both platforms help connect borrowers with participating lending partners.

Although the application process is similar, each platform works with its own lending network. As a result, the lenders available, eligibility criteria and loan offers you receive may differ.

| Feature | LoanConnect | FatCat Loans |

|---|---|---|

| Direct lender | No | No |

| Online application | Yes | Yes |

| Loan comparison platform | Yes | Yes |

| Personal loans | Available through participating lenders | Available through participating lenders |

| Bad credit options | Available through some lenders | Available through some lenders |

| Debt consolidation loans | Available through some lenders | Available through some lenders |

| Lending decisions | Participating lenders | Participating lenders |

| Funding | Provided by the approved lender | Provided by the approved lender |

Whether you choose LoanConnect, FatCat Loans or another comparison platform, it’s always worth reviewing multiple loan offers before making a borrowing decision. Comparing the APR, repayment schedule, fees and total borrowing cost can help you identify the option that best fits your budget.

LoanConnect Customer Reviews

Customer experiences with LoanConnect vary. Because LoanConnect connects applicants with third-party lenders, some reviews may relate to the lender that handled the application rather than LoanConnect itself.

When reading customer feedback, look carefully at whether the reviewer is describing:

- LoanConnect’s online application and matching process.

- The lender that reviewed or approved the application.

- The interest rate or repayment terms offered by the lender.

- Whether the applicant was successfully matched with a lending partner.

Customer reviews can provide useful context, but they should not replace a careful review of the loan agreement, APR, fees, repayment schedule and total borrowing cost.

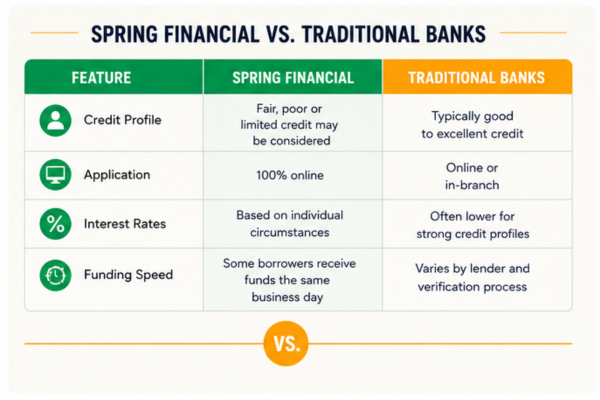

If you’re comparing Canadian financial services, you may also wish to read our reviews of easyfinancial, Spring Financial and Mogo.

Is LoanConnect Legit?

Yes. LoanConnect is a legitimate Canadian loan comparison platform that connects borrowers with participating lenders. It is important to remember that LoanConnect does not lend money directly or approve loan applications itself.

Any lending decision, loan agreement, interest rate and repayment terms are determined by the participating lender that reviews your application.

Before accepting any loan, review:

- The Annual Percentage Rate (APR).

- The total borrowing cost.

- Your repayment schedule.

- Any applicable fees.

- Whether the repayments comfortably fit your monthly budget.

You can also review the Financial Consumer Agency of Canada guidance on personal loans before applying for any credit product.

LoanConnect Alternatives

LoanConnect is one of several loan comparison platforms available to Canadian borrowers. Comparing multiple services may help you identify lenders, borrowing costs and repayment terms that better suit your financial circumstances.

Depending on your needs, you may also wish to compare:

- FatCat Loans.

- Traditional banks.

- Credit unions.

- Other online lenders.

- Specialist bad credit lenders.

Our Canadian lender reviews compare many of Canada’s best-known lenders and loan comparison platforms.

Is LoanConnect Right for You?

LoanConnect may be suitable for borrowers who prefer comparing multiple lending options through a single online application rather than applying individually with several lenders.

However, because LoanConnect is a comparison platform rather than a lender, the loan offers you receive depend entirely on the participating lenders that review your application.

Comparing several loan comparison services and lenders before applying can improve your chances of finding a loan with competitive pricing, suitable repayment terms and repayments that comfortably fit your budget.

How We Review Loan Comparison Platforms

Our reviews are based on publicly available information, lender disclosures, application processes, available loan products, consumer protections and independent customer feedback where available. We regularly review our content to reflect significant changes to lending platforms and help Canadian borrowers make informed financial decisions.

Frequently Asked Questions

Is LoanConnect a direct lender?

No. LoanConnect is not a direct lender. It is an online loan comparison platform that connects eligible borrowers with participating lenders that may offer personal loans and other credit products.

Does LoanConnect guarantee loan approval?

No. Submitting an application through LoanConnect does not guarantee approval. Each participating lender assesses applications using its own eligibility criteria, affordability assessment and verification process.

Can I apply with bad credit?

Some participating lenders may consider applicants with less-than-perfect credit histories. Approval is never guaranteed and lenders may also consider income, affordability, existing debt obligations and employment status.

How quickly can I receive a lending decision?

Decision times vary depending on the lender reviewing your application. Some lenders may provide an initial decision quickly, while others may require additional verification before making a final lending decision.

Does LoanConnect charge borrowers a fee?

LoanConnect does not set the interest rate or lender fees attached to a loan offer. Fees may apply through the participating lender and can vary by lender, loan product and province or territory. Before accepting an offer, review the loan agreement for administration fees, optional insurance, NSF fees and any other charges included in the total borrowing cost.

Will applying through LoanConnect affect my credit score?

The type of credit enquiry performed depends on the participating lender reviewing your application. If you’re unsure how different credit enquiries work, read our guide to soft vs hard credit checks in Canada. You can also learn more about Canadian credit reports from Equifax Canada.

Is LoanConnect better than applying directly with a lender?

That depends on your circumstances. A loan comparison platform can save time by allowing you to compare potential lending options through one application, while applying directly with a lender may be suitable if you already know which lender you wish to use.

How does LoanConnect compare with FatCat Loans?

Both LoanConnect and FatCat Loans are loan comparison platforms rather than direct lenders. Each works with its own lending network, so available loan offers, eligibility criteria and borrowing options may differ.

Final Verdict

LoanConnect provides Canadian borrowers with a convenient way to compare potential loan offers through a single online application. Because it operates as a loan comparison platform rather than a direct lender, all lending decisions, interest rates, fees and repayment terms are determined by the participating lender that reviews your application.

As with any borrowing decision, comparing multiple loan offers, reviewing the Annual Percentage Rate (APR), understanding the total borrowing cost and ensuring the repayments fit comfortably within your budget are essential before accepting any loan.

If you’d like to compare additional borrowing options, explore our Canadian lender reviews, or compare loan offers through FatCat Loans.

The FatCat Loans Editorial Team delivers clear, accurate, and unbiased guidance on loans, credit, and personal finance in Canada. Our writers follow strict editorial standards to ensure every article is trustworthy, well-researched, and easy to understand, helping readers make confident financial decisions.